Callon Petroleum's 6.375% Sr Notes due 2026

Bid 90.5 (YTW of 8.6%) | Target 100.0 (YTW of 6.4%)

Investment Highlights: Callon Petroleum (“CPE” or the “Company”) is an independent E&P Company based in Houston, TX with operations primarily in the Permian and Eagle Ford Shale.

The Company entered the Permian Basin in 2009 and was a pure-play Permian operator from 2013 to 2019, when it gained exposure to the Eagle Ford Shale following the merger with Carrizo Oil & Gas. As of FYE20, Callon had proved reserves of 476 mmboe, of which, 61% is oil. Average daily production was 81 mboe/d in 1Q21.

We recommend going long Callon’s 6.375% Sr Notes due 2026 which currently trades ~90.5, with a yield-to-worst (“YTW”) of ~8.6% (~450bps wider than the Barclays Corp HY Index and ~380bps wider than the E&P HY Index).

The 2026s provide incremental yield relative to its comps with manageable risks that the Company is actively working to mitigate in the near term.

Callon’s bonds have been trading below par as result of the COVID & OPEC/Russia related collapse in commodity prices occurring only a few months after the Company closed on its merger with Carrizo O&G on December 20, 2019. The completion of the merger resulted in elevated PF leverage that was intended to be reduced over 2020 through non-core asset sales and increased FCF generated through the realization of merger related cost synergies.

We believe that Callon will outperform on synergies and the global economic recovery will support favorable commodity prices, allowing Callon to reduce total debt while funding modest growth. Catalysts to bond price improvement can include one or more of the following:

Continued asset divestitures: Callon is actively working on divesting non-core assets inherited from Carrizo. This includes their Eagle Ford assets that produce ~22.9 mboe/d (76% oil), which if sold, could achieve a valuation up to ~$800mm based on recent transactions. Proceeds could be used to retire the 2023s and further reduce the RBL outstandings.

Continued FCF generation focused on debt reduction: Given the rapid recovery in commodity prices supported by strong underlying demand recovery, the Company is prioritizing FCF to reduce total debt.

A ratings upgrade in the near term would enhance access to capital markets and accelerate the refinancing of near-term maturities: The agency’s current ratings have been in place since before the release of 4Q20 results, and thus do not reflect the improved commodity price outlook nor the recent asset divestitures. If Callon is upgraded in the near term, it would accelerate their plans to refinance the 2023’s.

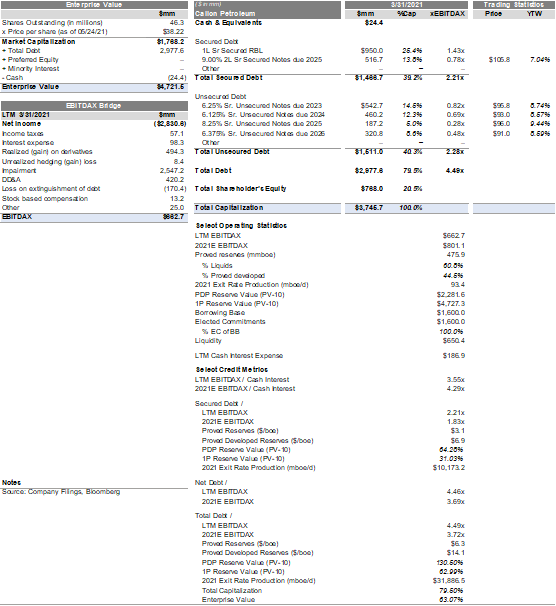

Current Capitalization

1Q21 Commentary

Note: The Company, along with the broader E&P industry, was negatively impacted in 1Q21 as a result of Winter Storm Uri which occurred in February. This period of extreme cold temperatures required a large portion of the Company’s production to be temporarily shut-in. Callon has since brought 100% of the impacted wells back online.

During 1Q21, Hedge adj revenue decreased ~5.5% y/y to $298mm vs $315mm during 1Q20 as a result of the following:

~19.7% decrease in daily production to ~81 mboe/d during 1Q21 vs ~101 mboe/d during 1Q20. The decrease in production was primarily due natural decline and producing wells being temporarily shut-in during February as a result of Winter Storm Uri.

$62.3mm in realized losses from the unfavorable effects of the Company’s commodity hedges.

The negative effects mentioned above were partially offset by a 19% improvement in pre-hedge realized commodity prices (~$40.9/boe during 1Q21 vs ~$34/boe in 1Q20).

Lease operating expenses (“LOE”) decreased ~2.6% y/y on a per barrel basis to $5.55/boe during 1Q21 vs $5.70/boe in 1Q20 due to the Company’s continued efforts to further improve overall efficiencies after the addition of Carrizo's producing assets, partially offset by the distribution of fixed costs over lower overall production.

Gathering & transportation expenses increased ~57.7% y/y to $2.47/boe during 1Q21 vs $1.57/boe during 1Q20, primarily due to oil transportation agreements which were entered into after 1Q20.

Cash G&A increased ~2.6% y/y on a per barrel basis to $0.88/boe during 1Q20 vs $1.68/boe during 1Q19, primarily resulting from the increased production and headcount reductions after the merger with Carrizo.

EBITDAX decreased to ~$171mm during 1Q21 vs ~$217mm in 1Q20, as a result of the above.

Leverage increased on an LTM basis to 4.5x at 3/31 vs 4.2x at FYE20 given the lower LTM EBITDAX vs FYE20, however we expect leverage to resume its trend lower in future quarters. We note that the total leverage test of <4.0x Total Debt / EBITDAX under the RBL has been suspended until 1Q22. The Company is still beholden to a <3.0x Secured Debt / EBITDAX covenant.

Liquidity remains adequate at $650mm at 3/31 consisting of $24.4mm of cash and $626mm of availability under the Company’s RBL which currently has $1.6bn of elected commitments.

Recent Asset Sale: After the quarter, Callon sold certain non-core properties in the Delaware Basin and received gross proceeds of $40mm. The Company will use the net proceeds to continue CPE’s debt reduction strategy.

Model Output

Asset Value & Recovery Analysis

We ran an EV analysis on Callon using both an NPV approach and a market-based approach to derive a total EV of ~$4.4bn. Our NPV analysis on the reserves used a 10% discount rate and price deck used in the financial model. This resulted in a total 1P reserve valuation of $4.72bn, with a PDPs making up ~$2.28bn (or ~48%) of that total.

In normal market conditions, Callon should be able to receive a bid for an amount close to our 1P valuation. In that scenario, we would recover 100%. If the company were to focus all their net cash flow to debt repayment, the 1P reserves would repay all outstanding debt within 7 years, or 29% of its economic life.

In our market-based approach, we used EV/EBITDAX multiple to derive an implied EV of $4.1bn. This is based on our 2022E EBITDAX estimate of $1bn, and a 4.0x multiple from the peer median of comparable companies.

In a liquidation scenario with a weak A&D market, a potential buyer may only be willing to pay for PDP reserves. In this downside scenario, we would recover ~56%.

Reserve Valuation

EV / EBITDAX Valuation